Understanding Income Types:

In order to optimize assets, minimize taxes, and empower authentic wealth, it is important to understand the different types of income and their tax implications.

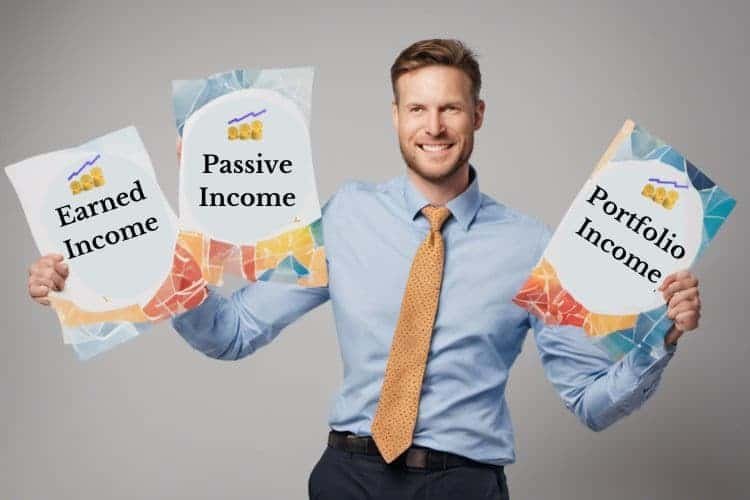

According to financial strategist and retirement planning specialist and one I have followed for over 15 years, Doug Andrew, there are three types of income that are subject to income tax: earned income, passive income, and portfolio income.

Earned income is what one earns through salaries or wages. This type of income is subject to income tax as well as FICA and Medicare taxes. Passive income, on the other hand, is income that is earned through rental properties or leasing and is not subject to FICA and Medicare taxes. Portfolio income includes interest, dividends, and growth on investments and is also not subject to FICA and Medicare taxes.

It is important to note that there is also a type of income that is tax-free and not subject to any of these three categories. This is where a properly structured and funded maximum funded indexed universal life insurance policy comes in. According to Andrew, if structured correctly and funded properly, this type of policy passes the liquidity, safety, and rate of return test with flying colors and is totally tax-free.

Some may wonder why this type of policy is tax-free. Andrew explains that the IRS actually dictates why it is tax-free under three sections of the Internal Revenue code. Despite concerns that the IRS may close this loophole, Andrew assures that it is unlikely as it has been in place since the 1986 tax reform act.

In summary, understanding the different types of income and their tax implications is crucial in making informed financial decisions. Earned income, passive income, and portfolio income are the three types of income subject to income tax, while a properly structured and funded maximum funded indexed universal life insurance policy can provide tax-free income.

The Concept of Maximum Funded Indexed Universal Life Insurance

Maximizing the funded indexed universal life insurance policy is one of the favorite financial vehicles of Doug Andrew, a financial strategist and retirement planning specialist. He has been helping thousands of people optimize their assets, minimize taxes, empower their authentic wealth, and accumulate money for long-term goals such as retirement.

When structured correctly and funded properly, a maximum funded indexed universal life insurance policy passes the liquidity safety rate of return test with flying colors and is totally tax-free. Three sections of the Internal Revenue Code dictate why it is tax-free, according to Doug Andrew. Since the 1986 tax reform, Americans pay income tax on only three types of income: earned, passive, and portfolio income.

Earned income is what people earn by working, usually in the form of salaries or wages. People have to pay income tax plus FICA (Federal Insurance Contributions Act) and Medicare taxes on earned income. Passive income is rental income from rental homes, apartments, equipment, or leasing, and people do not have to pay FICA and Medicare taxes on it. Portfolio income is interest, dividends, and growth on money inside investments, and people do not have to pay FICA and Medicare taxes on it.

A properly structured maximum funded indexed universal life insurance policy is not deemed earned, passive, or portfolio income, and people do not have to pay income tax on it. A maximum funded indexed universal life insurance policy, also known as a laser fund, is a liquid asset that can safely earn returns. It has six major advantages over a Roth IRA, which has only two advantages.

Doug Andrew recommends a maximum funded indexed universal life insurance policy over an IRA or 401k because it is not subject to tax on earned, passive, or portfolio income. It is a dream solution for a lot of financial goals because it is liquid, safe, and not at risk in the market. The returns are linked to what the market does using an index, but the money is not at risk in the market.

Advantages of the Laser Fund Over Traditional Investment Accounts

Benefits of the Laser Fund

A laser fund is a properly structured maximum funded indexed universal life insurance policy that passes the liquidity safety rate of return test with flying colors. It has six major advantages over traditional investment accounts such as IRAs or 401ks invested in the market. A laser fund is a dream solution for a lot of financial goals as it is liquid, safe, and tax-free.

Why Is the Laser Fund Tax-Free

The laser fund is tax-free because it is not deemed earned passive or portfolio income when money is taken out of the policy. The Internal Revenue Service (IRS) dictates why it is tax-free under three sections of the Internal Revenue code. The cost of insurance is the only cost that the policyholder has to pay, which is around one percent of the rate of return.

The Use of Laser Funds in Various Financial Goals

A laser fund is a versatile financial vehicle that can be used for various financial goals. It can be used as working capital for business, an emergency fund, or as an accumulation vehicle for long-term goals such as retirement. The policyholder can access the money in a few days through electronic funds transfer, making it a convenient option for many.

The Concept of Indexing

A laser fund uses indexing to link the returns to what the market does. The policyholder’s money is not at risk in the market, but they can benefit when the market goes up. This makes it an attractive option for those who want to earn a rate of return without risking their money in the market.

In summary, a laser fund has several advantages over traditional investment accounts. It is tax-free, versatile, and safe, making it a dream solution for many financial goals. The use of indexing also allows policyholders to earn a rate of return without risking their money in the market.

Accessing Money from a Maximum Funded Insurance Contract

A properly structured maximum funded indexed universal life insurance policy can be a great financial vehicle for long-term goals such as retirement. Doug Andrew, a financial strategist and retirement planning specialist, explains that if it is structured correctly and funded properly, it passes the liquidity safety rate of return test with flying colors and it’s totally tax-free.

Many people wonder why it’s tax-free. According to Doug, the IRS dictates why it’s tax-free under three sections of the Internal Revenue code. The laser fund, which is a properly structured maximum funded indexed universal life insurance contract, is an acronym that stands for liquid assets safely earning returns. Doug explains that it really knocks the socks off of most investment accounts like IRAs or 401ks invested in the market and a lot of other investments.

A laser fund has six major advantages, compared to a Roth that only has two. Doug recommends a laser fund because the money you take out of it is not deemed earned passive or portfolio income. As a result, it’s totally tax-free.

Doug recommends that people keep their serious cash accumulated and on deposit inside a portfolio of laser funds. This is because laser funds are totally tax-free and knock the socks off of IRAs or 401ks. They are working capital for business, an emergency fund, and a dream solution for a lot of financial goals.

Doug adds that a maximum funded indexed universal life insurance policy is the brainchild of EF Hutton back in 1980. They realized that some of the best financial money managers in the world are the multi-trillion dollar insurance companies and Industry. They’re the backbone of America and the backbone of the world, having weathered the Great Depression with flying colors.

Insurance Companies as Financial Money Managers

Insurance companies have become one of the most reliable financial money managers in the world. According to Doug Andrew, a financial strategist and retirement planning specialist, insurance companies are the backbone of America and the world. They have weathered the Great Depression with flying colors and have proven to be a safe haven for investors during times of economic turmoil.

One of the most popular financial vehicles that insurance companies offer is a properly structured maximum funded indexed universal life insurance policy. This policy, if structured correctly and funded properly, passes the liquidity safety rate of return test with flying colors and is totally tax-free.

Many people wonder why this policy is tax-free. According to Andrew, the IRS dictates that it is tax-free under three sections of the Internal Revenue code. Since the 1986 tax reform, there are only three types of income that Americans pay income tax on: earned, passive, and portfolio income. Income that is none of these three is totally tax-free.

Earned income is what people earn by working, usually in the form of salaries or wages. When people earn this type of income, they have to pay income tax plus FICA, Social Security, and Medicare. Passive income, on the other hand, is rental income off of a rental home or rental apartments or rental equipment or leasing. Portfolio income is interest and dividends and the growth on money inside of investments.

A laser fund is a properly structured maximum funded indexed universal life insurance contract that is not deemed earned, passive, or portfolio income. This is why the money taken out of a laser fund is not subject to income tax. In fact, a laser fund has six major advantages over a Roth IRA, which only has two advantages.

By using a laser fund, people can accumulate their money for long-term goals such as retirement. It is a dream solution for a lot of financial goals because it is totally tax-free, liquid, and safe. It is also an emergency fund and working capital for business. Since the money is not at risk in the market, people do not lose when the market crashes. Instead, they benefit when the market goes up.

The Role of Banks in the Financial Ecosystem

Banks play a crucial role in the financial ecosystem by providing financial services to individuals and businesses. They act as intermediaries between savers and borrowers, facilitating the flow of funds in the economy. Banks accept deposits from individuals and businesses and use these funds to make loans to other individuals and businesses. This process of borrowing and lending is essential for economic growth and development.

One of the primary functions of banks is to provide loans to individuals and businesses. Banks offer a variety of loans, including personal loans, business loans, and mortgages. These loans help individuals and businesses to finance their projects and achieve their goals. Banks also provide credit cards, which allow individuals to make purchases and pay for them over time.

Banks also offer a range of deposit accounts, including checking accounts, savings accounts, and certificates of deposit. These accounts provide a safe place for individuals and businesses to store their money and earn interest on their deposits. Banks also offer other financial services, such as investment advice, insurance, and wealth management services.

In addition to their role as intermediaries between savers and borrowers, banks also play a critical role in the payment system. Banks facilitate the transfer of funds between individuals and businesses, allowing for the smooth functioning of the economy. Banks also issue credit and debit cards, which allow individuals to make purchases and access their funds.

Overall, banks are an essential part of the financial ecosystem. They provide a range of financial services that help individuals and businesses to achieve their goals and contribute to economic growth and development.

Recent Posts

Experian Boost is a free credit-building tool that can help improve your credit score. It works by allowing you to add positive payment history for bills that are not traditionally reported to credit...

In today's society, many individuals are realizing that the traditional path of going to school, getting a job, and saving for retirement may not lead to the fulfilling life they desire. They may...